Need a faster way to check borrowing options in South Korea without starting at a crowded branch counter. Hana Card is often part of that conversation because Hana’s ecosystem combines card services, app-based account tools, and loan-related features inside a mobile-first flow.

For many applicants, especially foreign residents with stable jobs, the process can feel simpler when eligibility is checked early, and documents are prepared before opening the app. A smooth result still depends on your profile, not the app alone.

Employment history, visa status, card usage, salary records, and branch-level discretion can all affect the outcome.

That is why the smartest approach is a practical one: confirm what Hana Pay shows, prepare proof in advance, and treat branch guidance as the final decision point.

Why Hana Card Is Often Considered For Personal Borrowing

Hana Card sits inside a broader Hana Financial ecosystem, which matters when convenience is the main priority. Hana’s card app and related banking apps are built around mobile access, so applicants can check balances, limits, transaction history, and some finance services without switching to a paper-heavy process.

A person already using Hana services may move faster through identity checks and service navigation because the account and card relationship already exists. Hana Card also presents finance menus that include loan-related functions, reducing friction for people who prefer an app-first approach over repeated branch visits.

Hana Bank has a long reputation for serving international customers in Korea through selected branches and English support channels, which can make follow-up steps easier when a digital application needs manual review.

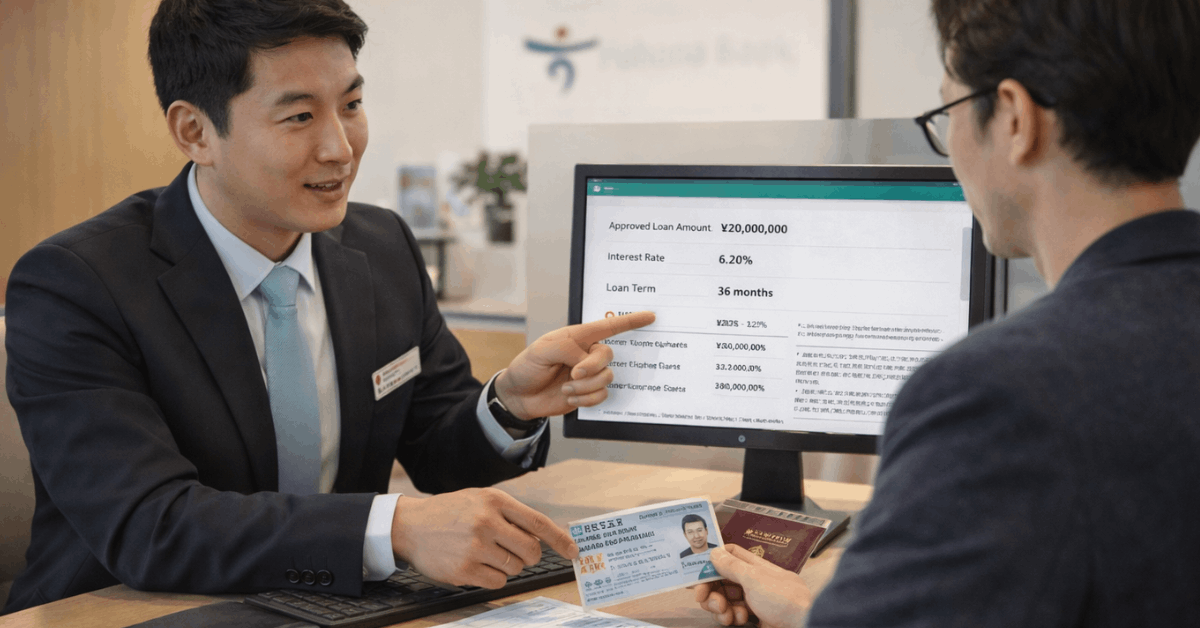

What “Personal Loan” Means In The Hana Card Context

Loan terminology can get confusing because card-based borrowing and bank credit loans are not always the same product. Hana Card materials and app menus commonly separate short-term and longer-term card borrowing functions under finance services, so product labels matter before any application starts.

A typical Hana Card loan application path may involve one of these categories:

- Short-term card loan (cash service), which functions like a cash advance linked to the card and usually carries different pricing and repayment conditions than a standard installment loan.

- Long-term card loan (card loan), which is a broader card-linked borrowing option offered through Hana Card finance services, is subject to eligibility and internal screening.

- Bank-side personal credit loan, which may be handled through Hana Bank channels, sometimes requiring branch consultation even if discovery starts on mobile.

Confusion usually happens when applicants assume every “loan” button in the app is the same. Product type affects limits, repayment structure, and how suitable the option is for a short cash gap versus planned borrowing.

How The Hana Pay App Supports The Application Process

Digital convenience is one of the strongest reasons people start here. Hana Card’s app materials describe a service structure that lets members review payments, limits, recent transactions, and finance menus on a smartphone, which supports pre-application preparation and post-approval management.

The Hana Pay app loan workflow is useful even when final approval requires a human review. Mobile access helps you verify account activity, check available services, and complete authentication steps used for sensitive functions. Hana Card also notes that some services require card authentication or mobile authentication for safer transactions, which is common in Korean financial apps.

The app is not only for borrowing. Hana Pay is also built for payment and account visibility, which gives lenders more context when evaluating active users. A cleaner transaction history and stable salary deposits can help your file look easier to review, especially when income consistency matters.

Basic Eligibility Signals That Often Matter

Approval rules can vary by product, branch, and applicant profile, so no single checklist guarantees a result. Still, recurring patterns appear in foreign resident applications, and preparing around those patterns saves time.

Foreign applicants often report stronger outcomes when these conditions are already in place:

Stable Residency Status and ARC Validity

A longer remaining period on the Alien Registration Card can matter because lenders want enough legal stay period to match repayment risk. Reports commonly mention a preference for meaningful remaining validity, and branch staff may review visa category and expiration date closely during screening.

Employment Continuity and Insurance Records

Korean lenders often rely on formal employment verification signals, not verbal explanations.

A stable employer history and enrollment in the 4 major insurances Korea loan context can support credibility because it shows regular payroll and social insurance linkage. Some applicants report being asked for longer employment continuity, especially when applying as a foreign resident.

Income Traceability

Salary paid into a bank account creates a clean review trail. Visible salary deposit records in Korean history can make it easier for staff to verify consistency than cash-based or irregular income patterns. Applicants using one primary payroll account usually have an easier time gathering evidence.

Document Checklist To Prepare Before You Apply

Document readiness is where many applications slow down. A strong file usually wins on clarity, consistency, and matching names across records.

- A practical foreigner loan documents Korea checklist often includes:

- ARC (Alien Registration Card)

- Proof of residency, sometimes requested through local tax office documentation

- Proof of employment, including records tied to the National Pension Service when requested

- Recent salary deposit history, often covering at least six months

- Additional income or insurance contribution proof for freelancers or nonstandard employment cases

Freelancers and mixed-income workers usually need extra support documents. Proof of National Health Insurance Service contributions can help show ongoing local economic activity when a standard payroll trail is weak.

Naming consistency matters more than many applicants expect. Passport spelling, ARC name formatting, and bank account records should align as closely as possible to reduce manual review delays.

Foreigner-Specific Challenges and How To Reduce Them

Some foreign residents get approved smoothly, while others face requests that feel stricter than expected. That gap usually comes from differences in branch policies, visa types, employment profiles, and internal risk scoring rather than from a single yes-or-no rule.

A common hurdle appears when branch staff want stronger evidence of repayment capacity.

Applicants sometimes report requests for higher annual income levels or proof of assets, especially for unsecured borrowing. Those requests may feel inconsistent across locations, yet they reflect local review discretion and product-specific risk standards.

Practical steps can improve your odds without forcing a risky application:

Start With A Foreign-Friendly Hana Branch

A branch familiar with international customers can handle document review more efficiently. A KEB Hana foreigner branch with experience in employer-linked cases may also understand the paperwork patterns tied to your visa and payroll setup.

Use Your Employer Relationship If Available

Payroll-linked banking relationships often help the conversation move faster. A Hana Bank branch relationship tied to your employer can make verification easier because staff may already recognize the company’s payroll process and standard documents.

Apply Only After The File Is Clean

Timing matters. Missing insurance records, short salary history, or an ARC close to expiry can trigger avoidable declines. Cleaning those gaps first often produces a better result than testing the system too early.

Step-By-Step Application Flow That Usually Works Best

A clean sequence reduces errors and repeat visits. Most applicants get better results when they treat the app as a screening and management tool, then escalate to a branch only if required.

- Confirm your Hana Card membership status and app access on a supported smartphone.

- Review the finance menus and check which loan services appear in your account.

- Gather your ARC, employment proof, residency proof, and salary records before submitting anything.

- Match your personal details across documents and bank records.

- Submit through the app if eligible, or visit a branch when the service redirects you to in-person review.

- Recheck repayment terms, fees, and product type before accepting the final offer.

That sequence keeps the process organized and reduces the chance of accepting a product that does not match your actual need.

Final Takeaway On Hana Card Personal Loan Applications

Hana Card can be a practical starting point for personal borrowing in Korea when convenience, mobile access, and faster service checks matter.

The app supports a smoother experience, but approval still depends on employment stability, residency status, documentation quality, and product-specific screening.

A prepared applicant usually has a better experience than a rushed one, especially in foreign resident cases, where branch review can still decide the outcome.

Disclaimer

For the safest next step, check the current loan menu and conditions inside Hana Pay, then confirm final requirements at Hana Card or Hana Bank before submitting. Product terms, eligibility standards, and branch practices can change, so the latest official guidance should always override older forum advice.